Understanding Double Entry Book Keeping for Engineers and Coders

Della mercatura e del mercante perfetto by Benedetto Cotrugli, cover of 1602 edition; originally written in 1458 – localcopy / On Archive.org

Explanations of double entry book keeping by accountants lack the magic approach a good engineer uses. This explanation is by an engineer for an engineer that yields an intuitive understanding based on the modern concept of a database.

Research Links

- Wikipedia: Double-entry bookkeeping system

- Wikipedia: GnuCash

- Wikipedia: Summa de arithmetica – Luca Pacioli, a Franciscan friar and collaborator of Leonardo da Vinci, first codified the system in his mathematics textbook Summa de arithmetica, geometria, proportioni et proportionalità published in Venice in 1494

- Google: Summa de arithmetica pdf

- Archive.org: Summa de Arithmetica Geometria Proportioni et Proportionalità -in Italian

- Summa de Arithmetica Geometria Proportioni et Proportionalita – with side by side Italian and English for a few problems – not complete text

- Summa de Arithmetica Geometria Porportioni et Proportionalita – Double entry book keeping portion broken out / translated and interpreted

- Wikipedia: accounting equation

- So, you want to learn Bookkeeping! – tutorial

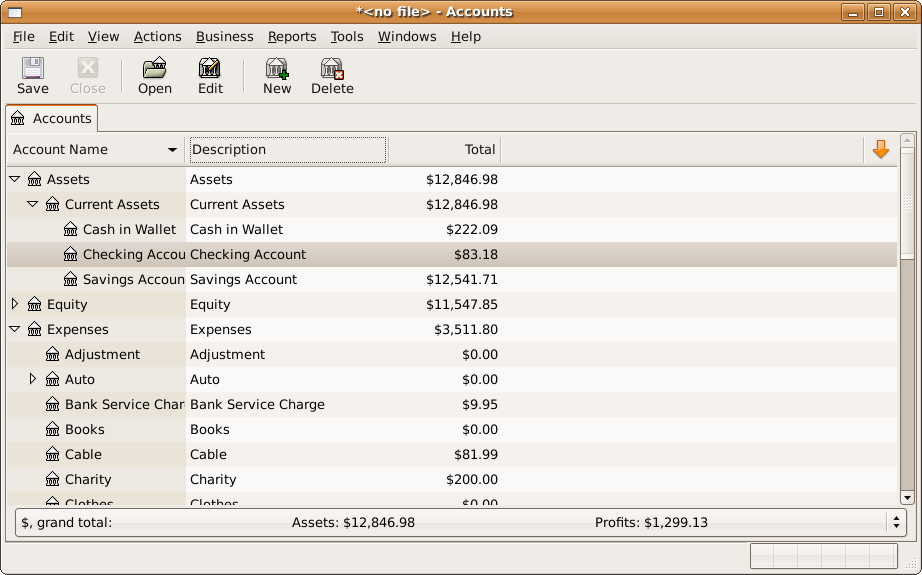

The image below is a screen capture from the program GnuCash. Note that there are various descriptive entries. One way of realizing that would be by using database tables. One could put all vehicular related expenses in a database table.

Imagine your busines has a bank account and you buy a 20000 dollar truck.

Your bank account goes down by 20000 dollar but your business now has a 20000 dollar asset.

Looking at things this way your business has not changed value. The contents have just changed form. Of course you might have sticker shock and not think this way. But for purposes of this process you have to think like an emotionless account or conversely a supremely confident person who sees that they made a decision to buy a tool and will stick with the process. A third way to look at things would be you are the head dictator of the government and all the business and workers are your minions. From that point of view the dictator owns all and thus money and vehicles just change location!

Now imagine it is the year 1300AD and you need to perform the same function using pen an paper as the GnuCash database does.

How would you go about that? First you would record transactions in a serial fashion like a diary. This is the quick and dirty record of transactions for on the spot recording with a customer right in front of you in your store.

Later you could take the days transactions and sort through them and place them in the correct tables. For instance when you purchased the vehicle you would enter it into your diary.

The Official Description of the Process

Successive Processes of the Double Entry System: Following are the successive processes of the double entry system:

- Journal: First of all, transactions are recorded in a book known as journal.

- Ledger:In the second process, the transactions are classified in a suitable manner and recorded in another book known as ledger.

- Trial Balance:In the third process, the arithmetical accuracy of the books of account is tested by means of trial balance. Read more about trial balance.

- Final Accounts:In the fourth and final process the result of the full year's working is determined through final accounts.

The first two steps are the serialized by hand sequence used to enter transactions into the books. The third and fourth are functions are evaluative functions of the books.

Double Entry BookKeeping Videos

These explanations show the mechanics but do not convey the intuition of the above explanation.

- YouTubeSearch: double entry bookkeeping

- YouTube: Double entry Book keeping explained in 10 minutes

- YouTube: Double entry bookkeeping Example – Patrick

0 Comments